Preface

To be clear, I don’t, in any way, begrudge the good fortunes of building product distribution company owners and CEO’s who have grown exceedingly wealthy through the process of building and expanding their respective companies. Personally, whether in the company of members of the Cargill-Macmillan family sharing dinner at Minnesota’s historic Lafayette Club, or offering assistance to a broke property owner who can’t afford to repair their storm damaged property because their P&C insurance company refused to pay their claim, I give little regard to the financial status of either party.

What I do however, give great regard to, is the apparent lack of concern and disregard on the part of building product distribution company owners and CEO's who seem to forget that, without the many thousands of hard working USA restoration general contractors who spend billions of dollars every year on purchasing the needed roofing and related building products from those building product distributors, none of the four owners / CEO's of the top four roofing and related building product distributors in the country would have ever been able to amass their combined nearly forty billion dollars of personal net worth.

My intent in creating this website is to both educate all of the interested parties - including National and International institutional and individual shareholder groups who have been invited to view this website, as well as bring back some much needed balance to a process that has, as will become apparent to all who read the following, gotten entirely off track. I begin by first outlining and defining...

The Problem

For Building Product Distribution Company Shareholders: Although unfamiliar with the realities of the property damage insurance restoration construction market and the multi-billion dollar sales "deficits" that the building product distributors operate under, without proper due diligence, investors readily buy into the promises made by building product distribution company M&A and C-Suite leadership of great things to come as they invest billions of dollars into acquiring typically smaller but related companies. While those acquisitions may dramatically increase the size of a building products distribution company's footprint (as well as their owners and CEO's personal bank accounts), it does nothing however to solve the problem of recapturing the billions of dollars-worth of annually missed building product sales which, when recaptured, would contribute mightily to helping the investors in those companies to achieve true maximum ROI. Until then, however...

The much hyped "Shareholder Value Maximization" model, which former GE CEO Jack Welch once called "the dumbest idea in the world", has become an outmoded model that no clear thinking investor who is paying attention will follow in today's changing investment environment.

For Building Product Distribution Company Corporate Leadership: The biggest mistake building product distribution company leadership makes is that they view the many thousands of contractors who spend billions of dollars on their products every year as customers. In reality however, they are not truly customers at all but are, rather, their "sales force" who orders then sells those billions of dollars-worth of building products and services to the real customers which are the commercial and residential property owners who need such products to complete all of the repairs to their damaged properties. Building product distribution companies spend millions of dollars on programs that may increase the efficiency of their contractor "sales force" product ordering and tracking processes, but they do nothing in the way of educating them on how the insurance claims recovery process should really work.

Not considering the above reality, rather than investing the relatively small amount of money needed to provide advanced and substantive training to their contractor "sales force" en masse which would result in a dramatic increase in sales of their building products to the ultimate buyers of those products, they instead operate under the assumption that, as long as the contractors keep ordering their products, there is no good reason to invest in getting available advanced and proven storm damage restoration process training into their hands. I suspect however, that as the institutional and individual investors in such companies become more educated on the subject matter as they now are as a result of our massive investor education support program, they will strongly disagree.

Building product distribution company owners, directors, and C-Suite executives: If you choose to continue to disregard the value and contribution that your many thousands strong contractor "sales force" brings to your business, as their awareness increases - as is now happening exponentially, they (as well as your investors) will likely soon choose to disregard you.

For Insurance Restoration Construction General Contractors: Through our concerted efforts, the many thousands of contractors from across the country are beginning to understand their true value and are now beginning to demand that, in return for the billions of dollars they already spend on building product distributors roofing and related products and the profits the distributors earn on those sales, clear thinking building product distribution company leadership who hope to retain their current contractor sales force base as well as grow it to record levels, will provide the needed insurance recovery process training to them.

For Insured Commercial and Residential Property Owners: Also tremendously harmed in the process, are the insured property owners who place their trust as well as hundreds of billions of dollars every year in premium payments, to the promises made to them by the P&C insurance industry that continues to fail them. Here's how one seasoned insured's plaintiff's attorney explained the problem several years ago;

“Despite the platitudes expressed by insurance companies in advertisements, where they brand themselves “the good hands people” or “a good neighbor,” they have one and only one purpose – to make as much money as possible. The way insurance companies make money is simple, by paying either nothing or as little as possible on any claim. What is fair or right is of no consequence.” Scott Dinsmore, APC (CA).

(Click on the picture above to see more evidence on YouTube)

![]()

Note to roofing and related building product manufacturers: All of the above also negatively affects your sales as well.

The Solution

The only restoration contractor training available on the planet that teaches the insurance covered restoration contracting process from the forty years of combined retail & restoration construction industry experience, insurance & investment industry advisory experience, and winning Pro Se legal industry experience perspectives of its creator.

As has been repeatedly proven over the years, storm and related damage restoration contractors who complete our advanced 3RSystems, LLC storm damage restoration contractor insurance claims process training program are able to regularly and powerfully defeat and overcome P&C insurance company representatives unfair attempts to underpay or deny their customers legitimate property damage claims. They are also able to dramatically increase the number of property damage restoration contracts they write each year and, to the great benefit of the building products distribution company that makes the investment in getting the training into their contractor "sales force" hands, repeatedly and dramatically increase their per contract building product orders as they dramatically increase their insured customers final claim settlements.

Proprietary 3RStimax© property damage repair estimation program

Prior to the year 2005, restoration contractors used a variety of different free market repair estimating programs to estimate the cost of repairs to their insured property owner customers damaged properties. Around 2005, the property & casualty industry introduced a repair pricing estimating program called Xactimate. Owned and controlled by the property & casualty insurance industry, they sold the program to restoration contractors as “the industry standard” repair estimating program. The biggest problem with that program however, is the fact that being owned and controlled by the property and casualty insurance industry, the repair pricing listed was and still remains below free market pricing which results in dramatic underpayments to insured property owners – in fact, billions of dollars-worth every year, as shown through the link below.

“Weaponizing Xactimate: The Insurance Industry’s Dirty Secret”

How was the property & casualty insurance industry able to, over the past twenty years, convince tens of thousands of restoration contractors from across the country to buy into the Xactimate (and Symbility/Cotality) “industry standard” myth? As new contractors entered the restoration construction market, they allowed themselves to be convinced that, as a result of aggressive marketing of Xactimate by property and casualty insurance industry leadership, using that “forced market”, knowingly and intentionally underpriced “industry standard” estimating program would move insurance company desk adjusters to more quickly approve the contractors repair estimates. Plus, they were afraid that, by implication, if they submitted their customer’s damage repair estimates on a platform that was not Xactimate (or Symbility/Cotality), their customer’s insurance claim settlements would be delayed.

Knowing better, having previously proven the Xactimate “industry standard” myth to be just that, when I introduced my advanced restoration contractor training program to the construction industry in 2010, I included my in house formulated real, true, and accurate (RTA) free market 3RStimax© contractor repair estimating program as an integral part of the program. Key to the success of 3RStimax© was the application of my non-insurance industry “industry standard” training that taught contractors how to overcome insurance company adjuster price objections before they were even presented.

The graph shown below clearly illustrates the dramatic difference in pricing between “industry standard” insurance company adjuster claim “final” offer(s) ($72,500) and the actual “Total claim recovery with 3RStimax©” ($270,214). Also key to note is the fact that, as a result of the contractors applying what they learned through the training, and submitting their estimates on 3RStimax© which were accepted and approved at the substantially higher real, true, and accurate (RTA) free market pricing shown, their insured customers were also able to avoid the costly and time consuming involvement of outside advisors.

(click on the graph to enlarge)

__________________________________________________________________________________

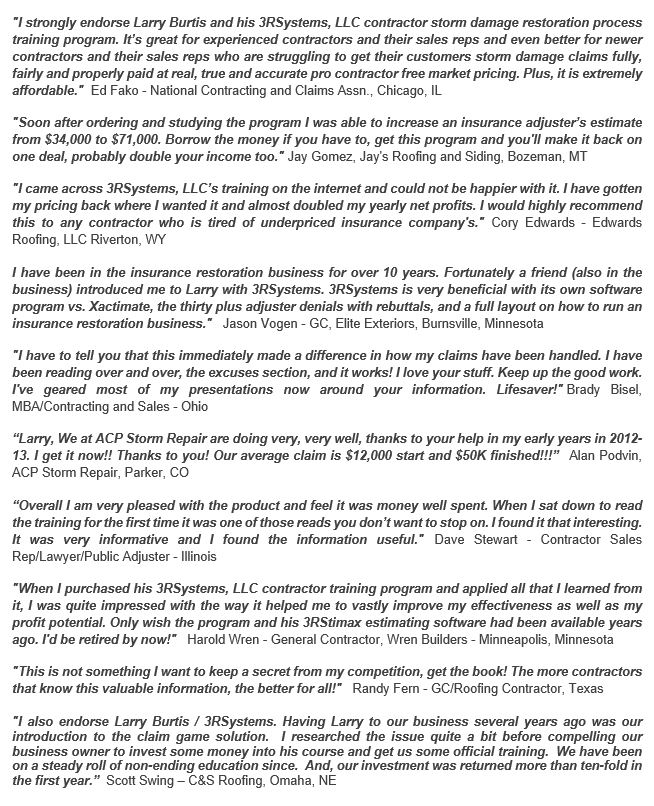

Praise for the 3RSystems, LLC Storm Damage Restoration Contractor Training Program

As a powerful example as proof of how the training has helped contractors from across the USA to successfully overcome the P&C insurance industry resistance and produce substantially improved results for themselves, their insured customers, and their building product distributors, financially and otherwise, review the pro contractor endorsements of the training program shown below.

__________________________________________________________________________________

Insured Commercial and Residential Property Owner Help

If you've suffered climate disaster damage to your commercial, residential or multi-housing property, you need our FREE:

3RS Insured Property Owners Storm Damage Recovery Guide©

Groups such as Organizing Resilience, United Survivors Disaster Relief (USDR), and many other like organizations contribute greatly to changing the mindset, the approach, and the response to climate caused disasters. Although, through such programs, victims are helped to eventually recover after a climate caused disaster, all too often these days, those same people are victimized a second time when they file claims with their property and casualty insurance companies who have promised to make them whole. As a result, far too many of those victims often find themselves waiting many months and even years - if ever, to achieve true and full recovery.

Part of the reason for that is the fact that property owners typically have no idea how the insurance claim recovery process really works - and the property and casualty insurance industry takes full advantage of that fact. In order to help millions of property owners from across the USA to overcome that knowledge deficit however, I wrote the above guide that gives them an in depth understanding on how the process should really work. By learning what is in the guide, property owners who study the guide are empowered to level the playing field when dealing with their insurance companies and avoid the intentional delay, deny, defend claim tactics that are placed in their way by wayward insurance adjusters and engineers. This also allows them to avoid the often quite costly and time consuming expense of having to hire outside help to move their legitimate property damage claims to fair, full, and final settlement.

Included in the guide is a chapter entitled "First things first – The Claims Process - from Filed to Final" that will teach readers of the guide the claims process steps in essentially the same manner that a 3RSystems, LLC trained restoration contractor would follow. This will allow insured property owners to effectively and powerfully deal directly with their insurance companies when their contractors no longer can because of UPPA and other unfair insurance industry lobbyist promoted prohibitions placed on them. The end result being that more claims are settled faster and at settlement rates more relative to the premium payments made by the insured's. Their contractors are then able to order all of the materials needed (billions of dollars-worth) from their building product distributors with which to complete all of the repairs.

3RS INSURED PROPERTY OWNERS STORM DAMAGE RECOVERY GUIDE© (PREVIEW)

___________________________________________________________________________________

BUILDING PRODUCT DISTRIBUTORS / INVESTORS

From V I S I O N to W I S D O M

The building products distributor who makes 3RSystems, LLC restoration contractor training available to all of their restoration contractor "sales force" across the country will, as shown below, advance their company product sales to record levels, take a #1 top level position in the building products distribution industry, and achieve true maximum ROI for themselves and their investors.

Question:

Who's really in charge and, which distributor (and their investor's) will win?

The Answer:

The distributor who provides their contractor customers with 3RSystems, LLC training.

The results...

![]()

Point of interest and food for thought

As recently posted on line…

“$23.5M in Funding to Build Out the End-to-End Roofing Software”

From the writer: “This investment will help accelerate the development and launch of groundbreaking roofing solutions, including our newly launched CRM, and soon-to-be-launched Payment Processing, Material Purchasing, and more." Participating in the investment which would accrue limited benefits to the distribution company behind the investment was ABC Supply Co. Inc. which is privately owned by founder and Chair Diane Hendricks - "the richest self-made woman in America" whose current personal net worth is over twenty-two BILLION dollars (Forbes - April 30, 2026).

While that quite substantial $23.5M investment may help roofing contractors to increase their work efficiencies such as material purchasing and delivery scheduling, it does not and cannot and, therefore, will not help them to solve the problems that, at a small fraction of the investment cost of the above mentioned program, the already developed and launched, and many years proven 3RSystems, LLC restoration contractor training powerfully solves for contractors who focus much of their work on insurance paid property damage repair and recovery contracting. With the proper contractor training, property owners would be better served, billions of dollars-worth of previously unordered roofing and related building products orders would be recaptured, and building product distribution company shareholders (both private and public) would be able to achieve substantially higher returns on their investments in those building product distribution companies.

Also missing the mark was Executive VP and CFO of The Home Depot, Richard McPhail, who, at the recent Modex 2026 supply chain strategy conference in Atlanta, called Home Depot’s supply chain “a strategic weapon — a $200+ billion e-commerce operation backed by hundreds of distribution facilities, same-day delivery capability, and a contractor-focused network spanning thousands of delivery branches. For contractors, this matters directly: the infrastructure being built is explicitly designed around your workflow — scheduled deliveries to jobsites, bulk material staging, and specialty trade supply — not just consumer convenience. Over half of our sales go to the professional contractor, McPhail said. Serving that customer with reliability and speed is critical." (SRS Distribution, Inc. is a wholly owned subsidiary of Home Depot).

Still however, as I pointed out to McPhail in a recent message, nothing was said regarding the value of contractor training that would exponentially advance the contractors ability to sell more product for more money and get more work done in much less time.

___________________________________________________________________________________

Distribution company leadership - the time to act is NOW!

As your institutional and individual investors become increasingly aware of the real world problems outlined on this website and elsewhere, they will be asking when you will be making the small but necessary investment into getting 3RSystems, LLC restoration contractor training into the hands of ALL of your valued contractor customer "sales force" who are the primary source of your profits as well as the source of their investment returns. To learn more about acquiring the program exclusively for your company, contact Larry through the Contact link shown at the top of this page.

Copyright © 1996 – 2026 ICCOA / 3RSystems, LLC Minneapolis, Minnesota USA All rights reserved